How Rewards Work in Credit Card Platforms | API-Based Incentives Explained

Remember, rewards are an engagement layer — Not a Core Banking Function

In modern credit card platforms, rewards do not live inside:

- Core banking systems

- Card network rails

- Settlement or clearing systems

Instead, rewards function as an event-driven engagement layer that reacts to user behaviour without touching sensitive financial data.

This separation is intentional and critical for:

- Security

- Compliance

- Faster iteration cycles

Common credit card reward triggers

Credit card platforms typically trigger rewards on:

- First successful card transaction

- Monthly spend milestones

- Category-based spends (fuel, travel, dining)

- EMI conversion events

- Utility & bill payments

- Dormant card reactivation

- Cross-sell actions (insurance, loans)

Triggers are configurable and can be adjusted without redeploying core systems.

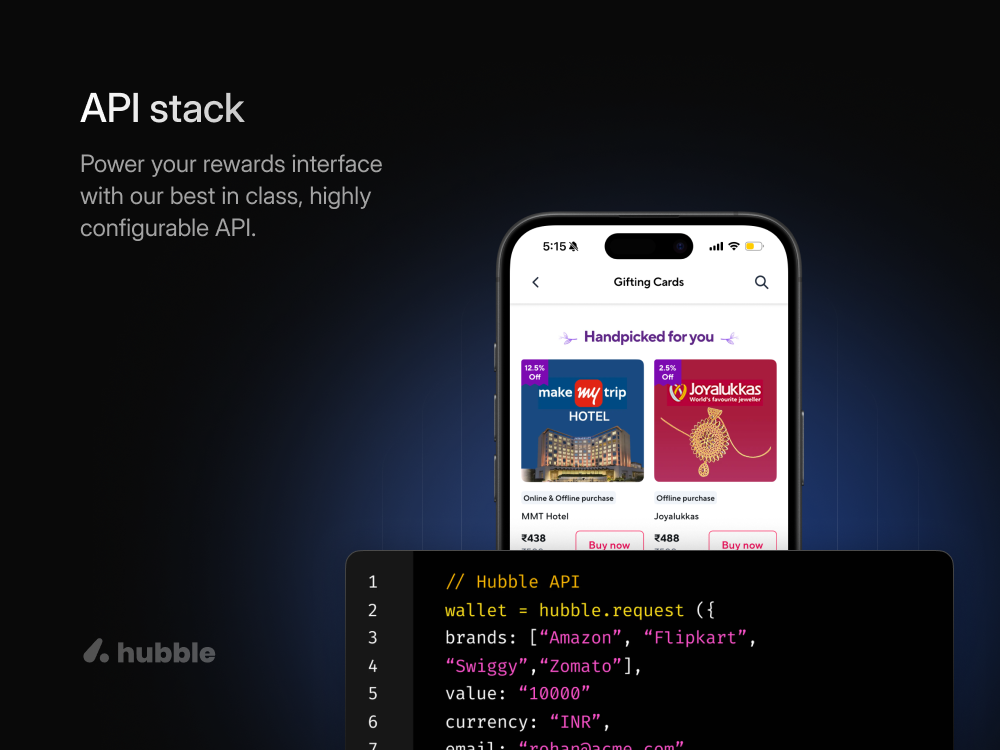

End-to-End Rewards Flow (API Model)

- A transaction or behaviour occurs inside your platform

- Internal rules engine evaluates eligibility

- A reward event is sent to Hubble via API

- Coins are credited instantly to the user wallet

- The user redeems a brand gift card on demand

At no point does Hubble receive:

- Card PAN data

- Settlement details

- Sensitive financial identifiers

This keeps rewards decoupled, auditable, and low-risk.

How to choose the right Issuance model

Real-time rewards

- Used for activation and engagement

- Higher perceived value

- Immediate behavioural reinforcement

Batch rewards

- Used for monthly milestones

- Lower system dependency

- Suitable for legacy stacks

Most platforms adopt a hybrid model.

Reward logic Is business logic. It has to align with business goals.

Typical rule parameters include:

- User eligibility (new vs existing)

- Spend thresholds

- Category inclusion/exclusion

- Frequency caps

- Cool-down periods

- Campaign start and end dates

Rules sit outside the card engine, enabling faster testing and budget control.

How Users Experience Rewards

Rewards appear inside:

- Existing credit card app UI

- Rewards or wallet section

- Post-transaction notifications

Users do not need a separate app or login.

Redemption remains embedded in the platform flow.

How Reward Abuse Is Controlled

Common safeguards include:

- Per-user reward caps

- Velocity throttling

- Device-level checks

- Transaction pattern monitoring

- Redemption anomaly detection

These controls operate independently from payment risk engines.

Why This Model Is BFSI-Safe

This architecture ensures:

- Zero card data exposure

- No impact on settlement flows

- Clear audit trails

- Simple RBI audit explanations

- Non-monetary reward classification

Short summary